by @Goldfinger on ceo.ca

Tax loss selling silly season is always an opportunity-laden time of the year in the junior mining sector. Between November and mid-December each year, investors typically have the opportunity to feast on bargain basement share price deals in already beaten down stocks. It’s the time of year when long term value goes out the window, and the opportunity to have a smaller tax bill takes precedence.

After a brutal year across the junior mining sector, this year’s tax loss silly season is poised to be particularly festive with dozens of stocks for sale on the clearance rack.

In May, Eagle Royalties (CSE:ER) was spun out from prospect generator Eagle Plains Resources (TSX-V:EPL). The idea behind the spin-out was to take most of the royalties that Eagle Plains has accumulated over the last 30 years, and create a dedicated royalty company. By creating the spinout it crystalized the value of EPL’s royalty portfolio, and made EPL more of a pure play prospect generator and geological contractor.

This is a sponsored post on behalf of Eagle Royalties Ltd.

In May, Eagle Royalties effectively raised C$3 million by issuing 10 million shares at $.30 each (including a $.50 warrant that is good for 24 months) and quietly began trading under the symbol ER on the CSE. Over the last five months, the share price has gradually been ground lower, reaching $.105 earlier this week. A 66% decline in the value of the company from a C$18 million market cap in June to a C$6 million market cap today. You are probably asking, “what has changed since June? Did ER drill some dusters or misplace a few million in its treasury?” – the answer to both questions is a resounding NO.

The only change since June has been deteriorating investor sentiment across the junior mining sector. This type of situation reminds me of an example my friend Bob Moriarty often uses; if a new car is for sale at $45,000 one day, and the following day you walk in and it’s suddenly been marked down to $15,000, what would you do? The answer is that you wouldn’t just buy one car, you’d buy two!

Let’s review the assets in Eagle Royalties:

- ~C$2.3 million in cash

- 50 royalty assets in Saskatchewan, British Columbia, and the Yukon Territory

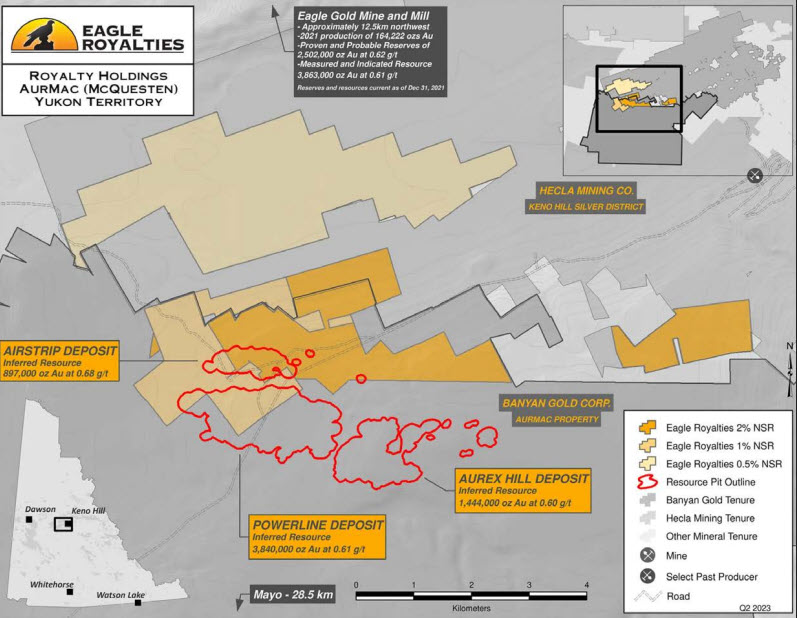

- Flagship asset = AurMac Royalty consisting of 1% and 2% NSRs covering all of Banyan Gold’s Airstrip Deposit and roughly 1/3 of its Powerline Deposit (AurMac Project)

- A dozen Athabasca Basin uranium royalties including projects held by Cameco, Denison, Orano and IsoEnergy

- Golden Triangle, BC and Keno Hill, Yukon royalties on projects owned by Skeena Resources and Hecla Mining

Some background on the Eagle Plains team will help to fully appreciate the opportunity available today. In the last twenty years, Eagle Plains Resources (TSX-V:EPL) has spun out more than $100 million in value via “dividends” (shares of spun-out companies). In total, there have been four spin outs, with Eagle Royalties being the fourth. Copper Canyon and Taiga Gold (which remained under the same management team that spun them out until the end) were eventually bought out at a premium by much larger companies, while Yellowjacket Resources (since renamed Dixie Gold) has recently announced a friendly merger with an Australian company. Will Eagle Royalties make it four for four?

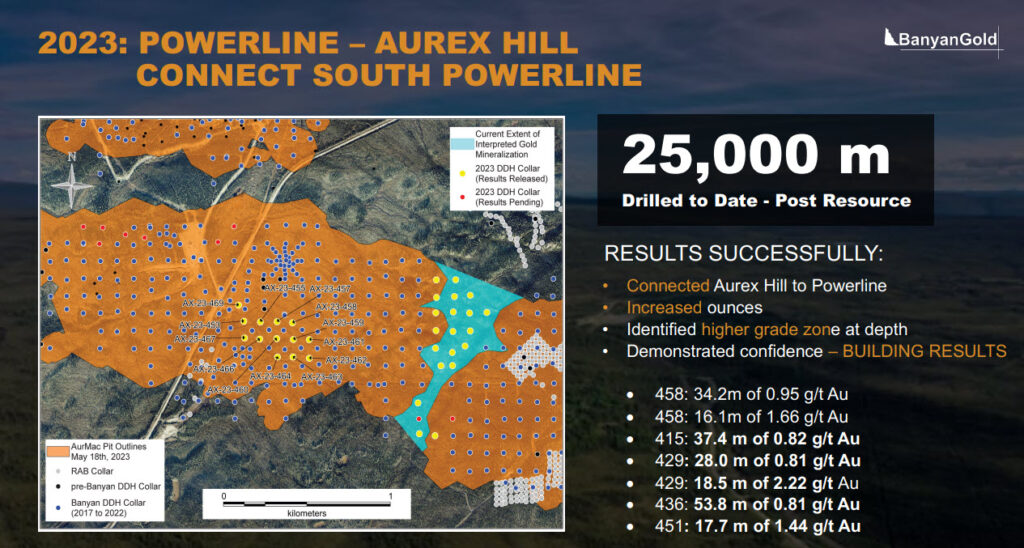

While we don’t know the answer to that question, we can better understand the potential by examining ER’s flagship AurMac Royalty. Banyan Gold’s AurMac Project hosts three proximal deposits (Airstrip, Aurex Hill, and Powerline) with inferred gold resources totaling 6.2 million ounces. AurMac is located in the Mayo Mining District of the Yukon that also hosts Hecla’s Keno Hill Mine and Victoria Gold’s Eagle Gold Mine. Banyan has quickly grown AurMac since its maiden drill program at Airstrip in early 2019, and the latest drilling in 2023 continues to expand the mineralized area in all directions:

The Powerline deposit is near surface and hosts consistent gold mineralization over a very wide area. Having connected the Powerline and Aurex Hill deposits in 2023 drilling, Banyan is still trying to find the edges of the gold mineralized zones.

Roughly 30% of the expansive Powerline Deposit (~4 million ounces grading .61 g/t gold) is overlain by claims subject to a 1% royalty held by Eagle Royalties. Meanwhile, the higher-grade Airstrip Deposit, which has a current Inferred Resource of 897,000 ounces of gold (.68 g/t gold), is entirely overlain by either a 1% or 2% NSR payable to Eagle Royalties.

When ER began trading in June, Banyan Gold shares were trading near $.40 (roughly C$120 million market cap). Since then, Banyan shares have declined ~30% to $.28 (C$84 million market cap).

BYN.V (Daily)

Banyan’s share price decline has likely reduced the ‘perceived value’ of ER’s AurMac Royalty holdings. However, the reality is that the value of ER’s AurMac Royalty depends upon a few factors that have little to do with Banyan’s month-to-month share price gyrations. The future price of gold, the permitting timeline and path to production at AurMac, and the size of any future mining operation are the real fundamental factors that investors should focus on when evaluating the value of ER’s AurMac Royalty.

As a longtime Banyan shareholder I believe that AurMac will be a producing mine one day, and due to the size of the deposit a 1% & 2% NSR could prove to be very valuable. For example, the nearby Eagle Gold Mine produces roughly 170,000 ounces of gold per year. At today’s gold price, a 1% NSR on 170,000 ounces of gold production per year would yield more than C$4 million per year payable to the royalty holder.

And that’s just for one year of production!

At today’s C$6 million market cap, with C$2.3 million in cash in its treasury, Eagle Royalties is priced as if it is on the clearance rack at the Dollar Store. Investors who can look ahead more than one month might be able to see the value available in ER shares today.

Disclosure: Author owns shares of Eagle Royalties at the time of publishing and may choose to buy or sell at any time without notice. Eagle Royalties Ltd. is a sponsor of Goldinger Capital. Readers are charged with conducting their own investment due diligence and recognize that micro cap stocks can deliver a 100% loss of invested capital.

DISCLAIMER: The contents of this article have been reviewed and approved by Eagle Royalties Ltd. The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. The companies mentioned in this article are high-risk venture stocks and not suitable for most investors. Consult company’s SEDAR profiles for important risk disclosures.

The author of this article is not a registered investment advisor and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions. This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.